add get involved

This commit is contained in:

commit

f1d5d403db

|

|

@ -1,22 +0,0 @@

|

|||

# Bitcoin is a means to counter authoritarian regimes

|

||||

|

||||

|

||||

## References

|

||||

* Bogost, Ian. 2017. ‘Cryptocurrency Might Be a Path to Authoritarianism’. The Atlantic 30.

|

||||

* Taleb, Nassim Nicholas. 2021. ‘Bitcoin, Currencies, and Fragility’. ArXiv:2106.14204 [Physics, q-Fin], July. http://arxiv.org/abs/2106.14204.

|

||||

* Krugman, Paul. 2022. ‘The Strange Alliance of Crypto and MAGA Believers’. The New York Times, 11 January 2022, sec. Opinion. https://www.nytimes.com/2022/01/10/opinion/crypto-cryptocurrency-money-conspiracy.html.

|

||||

* Xie, Rain. 2019. ‘Why China Had to Ban Cryptocurrency but the U.S. Did Not: A Comparative Analysis of Regulations on Crypto-Markets between the U.S. and China’. Wash. U. Global Stud. L. Rev. 18 (2): 457–89. https://openscholarship.wustl.edu/cgi/viewcontent.cgi?article=1684&context=law_globalstudies.

|

||||

* Wang, Gangjin, Yanping Tang, Chi Xie, and Shou Chen. 2019. ‘Is Bitcoin a Safe Haven or a Hedging Asset? Evidence from China’. Journal of Management Science and Engineering 4 (3): 173–88. https://doi.org/10.1016/j.jmse.2019.09.001.

|

||||

* Ottenhof, Luke. 2021. ‘Crypto-Colonialists Use the Most Vulnerable People in the World as Guinea Pigs’. VICE Media.

|

||||

|

||||

## References

|

||||

|

||||

* [@bogost_cryptocurrency_2017]

|

||||

* [@gerard_salvador_nodate]

|

||||

* [@analytica_salvador_2021]

|

||||

* [@gerard_salvadors_nodate]

|

||||

* [@murray_imf_nodate]

|

||||

* [@xie_why_2019]

|

||||

* [@kaiser_looming_2018]

|

||||

* [@wang_is_2019]

|

||||

* [@wang_blockchain_2020]

|

||||

|

|

@ -1,3 +0,0 @@

|

|||

# Are crypto assets a hedge against "debasement" of the dollar?

|

||||

|

||||

## References

|

||||

|

|

@ -1,11 +0,0 @@

|

|||

# Are crypto assets a hedge against inflation?

|

||||

|

||||

## References

|

||||

* Cembalest, Michael. 2022. ‘The Maltese Falcoin: On Cryptocurrencies and Blockchains’.

|

||||

* Shaffer, Daniel S. 2010. Profiting in Economic Storms: A Historic Guide to Surviving Depression, Deflation, Hyperinflation, and Market Bubbles. John Wiley & Sons.

|

||||

* Taleb, Nassim Nicholas. 2021. ‘Bitcoin, Currencies, and Fragility’. ArXiv:2106.14204 [Physics, q-Fin], July. http://arxiv.org/abs/2106.14204.

|

||||

* Wang, Gangjin, Yanping Tang, Chi Xie, and Shou Chen. 2019. ‘Is Bitcoin a Safe Haven or a Hedging Asset? Evidence from China’. Journal of Management Science and Engineering 4 (3): 173–88. https://doi.org/10.1016/j.jmse.2019.09.001.

|

||||

* Frisch, Helmut. 1983. Theories of Inflation. Cambridge University Press.

|

||||

|

||||

## References

|

||||

* [@cembalest_maltese_2022]

|

||||

|

|

@ -1,27 +1,64 @@

|

|||

# The Aspirations and Claims of Crypto & Web3

|

||||

Explore crypto and "web3" in terms of the claims made about it. These subclaims fall into six categories about different aspects of either technical, financial or political reconfiguration projects.

|

||||

|

||||

* What are the key high level problems, aspirations and hopes that crypto & web3 movement speaks to?

|

||||

* What are the specific claims made for crypto & web3?

|

||||

* What are the evaluations of those claims and evidence for them?

|

||||

#### Better Economy

|

||||

|

||||

* [Is bitcoin a currency?](/claims/is-bitcoin-currency.md)

|

||||

* [Are crypto assets a risk to the dollar?](is-threat-dollar.md)

|

||||

* [What type of asset is a crypto token?](is-type-of-asset.md)

|

||||

* [How do we value a crypto token?](is-valuation-model.md)

|

||||

* [Are crypto assets a systemic risk to the economy?](../claims/is-systemic-risk.md)

|

||||

* [Is bitcoin the basis for a new gold standard?](is-digital-gold.md)

|

||||

* [Are crypto assets a bubble?](../claims/is-bubble.md)

|

||||

* [Are crypto assets a form of gambling?](../claims/is-gambling.md)

|

||||

* [Are crypto tokens an inflation hedge?](is-hedge-inflation.md)

|

||||

* [Is private money a desirable system?](../claims/is-private-money.md)

|

||||

* [Is bitcoin compataible with ESG investing?](is-bitcoin-esg.md)

|

||||

|

||||

#### Better Society / Financial Inclusion

|

||||

|

||||

* [What consumer protections exist for crypto assets?](is-consumer-protections.md)

|

||||

* [Are crypto assets a form of predatory inclusion?](../claims/is-predatory.md)

|

||||

* [Is crypto a solution for the unbanked?](is-crypto-unbanked.md)

|

||||

* [Is crypto providing faster payment rails or better remittance services?](../claims/is-better-payments.md)

|

||||

* [Are NFTs are good for artists?](is-nfts-artists.md)

|

||||

* [What is the narrative economics of crypto assets?](is-narrative-economics.md)

|

||||

* [Are crypto assets legal?](../claims/is-legal.md)

|

||||

* [Are crypto tokens a negative-sum investment?](is-negative-sum.md)

|

||||

* [Why do people invest in crypto tokens?](is-why-invest.md)

|

||||

* [Why does crypto have such a weird subculture?](is-weird-culture.md)

|

||||

|

||||

#### Financial Liberty

|

||||

|

||||

* [Is an unregulated transnational payment rail even desirable?](is-transnational-payment.md)

|

||||

* [Are crypto tokens a hedge against the "debasement" of the dollar?](is-hedge-debasement.md)

|

||||

* [Are crypto tokens a means to counter authoritarianism?](is-authoritarianism.md)

|

||||

* [Can I raise money for my non-profit using crypto tokens?](../claims/is-raise-nonprofit.md)

|

||||

* [Can I do a crowdfunded equity raise for my company using crypto tokens?](../claims/is-raise-company.md)

|

||||

|

||||

#### Solving Public Goods Problems

|

||||

|

||||

* [Is crypto a means to fund public goods projects?](../claims/is-public-goods.md)

|

||||

* [Is bitcoin mining harmful to the environment?](is-environmental-footprint.md)

|

||||

* [Is crypto bringing about the "financialization of everything"?](../claims/is-hyperfinancialization.md)

|

||||

* [Is crypto a giant misallocation of resources with an enormous opportunity cost?](../claims/is-opportunity-cost.md)

|

||||

|

||||

#### Financial Innovation

|

||||

|

||||

* [Is the underlying technology of "blockchain" useful for non-monetary purposes?](is-blockchain-tech.md)

|

||||

* [Is web3 even a well-defined term?](is-well-defined.md)

|

||||

* [Is web3 green?](is-web3-green.md)

|

||||

* [Is web3 decentralized?](is-web3-decentralized.md)

|

||||

* [Is web3 the next generation of the internet?](is-new-internet.md)

|

||||

|

||||

#### Creative Destruction

|

||||

|

||||

* [Is web3 a means to dismantle the American tech hegemony?](../claims/is-disrupt-hegemony.md)

|

||||

* [Is web3 a means to rebuild the global financial system?](../claims/is-new-financial-system.md)

|

||||

* [Are crypto tokens a means to accelerate the collapse of capitalism?](../claims/is-collapse.md)

|

||||

|

||||

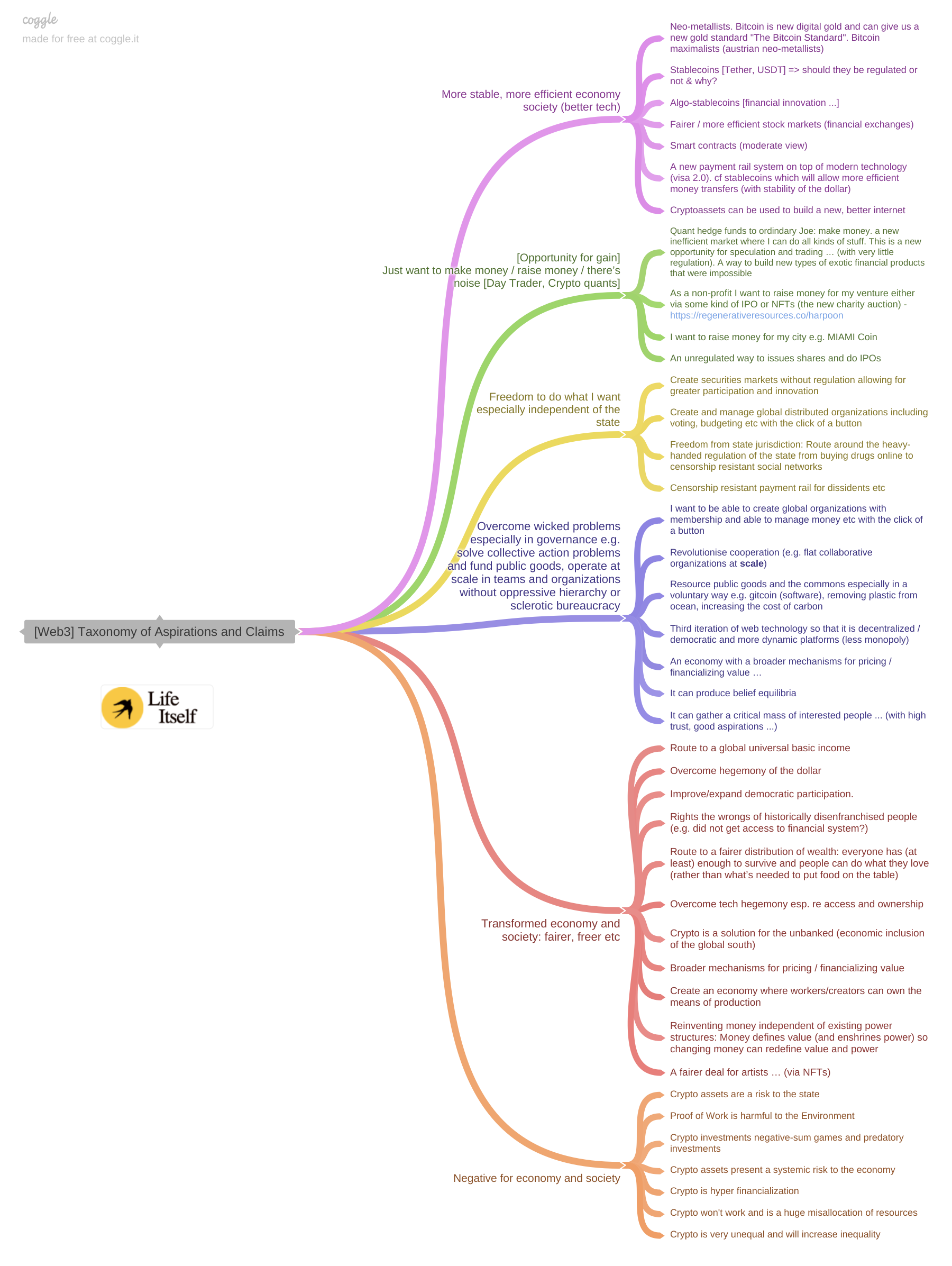

## Taxonomy of Aspirations and Claims

|

||||

|

||||

https://coggle.it/diagram/YhTzF8ZnKihmLdpm/t/web3-taxonomy-of-aspirations-and-claims

|

||||

|

||||

|

||||

|

||||

## TODO

|

||||

|

||||

#todo/writing #todo/clarify

|

||||

|

||||

* Aspirations and Claims: a short section explaining relationship of aspirations and claims

|

||||

* Web of claims: claims depend on other claims. We use hypothesis trees to break down claims

|

||||

* Claims vs questions: do we frame things as questions or statements e.g. Bitcoin is a currency vs Can Bitcoin function as a currency? Bitcoin harms the environment vs Does Bitcoin harm the environment?

|

||||

|

||||

## Subclaims

|

||||

|

||||

* How do we value a crypto token?

|

||||

* Are crypto assets a risk to the state?

|

||||

* What is the narrative of crypto assets?

|

||||

* Can Bitcoin function as a currency?

|

||||

* Are crypto tokens are securities (what type of assets are crypto token?)

|

||||

|

|

|

|||

|

|

@ -0,0 +1,21 @@

|

|||

# Bitcoin is not a means to counter authoritarian regimes

|

||||

Crypto assets are not a safe haven for one’s investments or a a shield against government tyranny. In his whitepaper *Bitcoin, Currencies, and Fragility*, Nassim Taleb writes of the "safe haven from tyranny" thesis:

|

||||

|

||||

> By its very nature, bitcoin is open for all to see. The belief in one’s ability to hide one’s assets from the government with a public blockchain easily triangularizable at endpoints, and not just read by the FBI but also by people in their living rooms, requires a certain lack of financial seasoning and statistical understanding — perhaps even a lack of minimal common sense. For instance a Wolfram Research specialist was able to statistically detect and triangularize "anonymous" ransom payments made by Colonial Pipeline on May 8 in 2021 — and it did not take long for the FBI to restore the funds. We can safely assume that government structures and computational power will remain stronger than those of distributed operators who, while distrusting one another, can fall prey to simple hoaxes

|

||||

>

|

||||

> [..] The slogan "Escape government tyranny hence bitcoin" is similar to advertisements in the 1960s extolling the health benefits of cigarettes.

|

||||

|

||||

The massive power asymmetries of authoritarian regimes and their control over both traditional payment rails and domestic implies that dissidents attempting to use crypto assets to circumvent repression or capital controls will find it very difficult to move assets or cash out. Without the capacity to cash out the efficacy of their actions is fundamentally limited to external geographic regions outside of the authoritarian regimes. Since no action can effected internal to the regime this fundamentally refutes the argument that crypto assets are an effective tool for dissidents.

|

||||

|

||||

This is best evidenced by the Canadian convoys in 2022 which attempted to take international donations in crypto assets and found themselves and their accounts frozen by both banks and Canadian [crypto exchanges](../concepts/crypto-exchange.md) which blocked transactions under [illicit financing](../concepts/illicit-financing.md) laws. This made using the donations to purchase supplies impossible and undermined the [crypto assets](../concepts/cryptoasset.md) narrative.

|

||||

|

||||

The complete ban of [crypto asset](../concepts/cryptoasset.md) by the People's Republic of China also does not lend credibility to the thesis that [crypto asset](../concepts/cryptoasset.md) are outside the remit of authoritarian controls and their restriction on capital movement and controls over domestic [money services business](../concepts/money-services-business.md).

|

||||

|

||||

## References

|

||||

1. Bogost, Ian. 2017. ‘Cryptocurrency Might Be a Path to Authoritarianism’. The Atlantic 30.

|

||||

1. Taleb, Nassim Nicholas. 2021. ‘Bitcoin, Currencies, and Fragility’. ArXiv:2106.14204 [Physics, q-Fin], July. http://arxiv.org/abs/2106.14204.

|

||||

1. White, Molly. 2022. ‘Cryptocurrency Off-Ramps, and the Shift towards Centralization’. Molly White. 12 February 2022. https://blog.mollywhite.net/off-ramps/.

|

||||

1. Krugman, Paul. 2022. ‘The Strange Alliance of Crypto and MAGA Believers’. The New York Times, 11 January 2022, sec. Opinion. https://www.nytimes.com/2022/01/10/opinion/crypto-cryptocurrency-money-conspiracy.html.

|

||||

1. Xie, Rain. 2019. ‘Why China Had to Ban Cryptocurrency but the U.S. Did Not: A Comparative Analysis of Regulations on Crypto-Markets between the U.S. and China’. Wash. U. Global Stud. L. Rev. 18 (2): 457–89. https://openscholarship.wustl.edu/cgi/viewcontent.cgi?article=1684&context=law_globalstudies.

|

||||

1. Wang, Gangjin, Yanping Tang, Chi Xie, and Shou Chen. 2019. ‘Is Bitcoin a Safe Haven or a Hedging Asset? Evidence from China’. Journal of Management Science and Engineering 4 (3): 173–88. https://doi.org/10.1016/j.jmse.2019.09.001.

|

||||

1. Ottenhof, Luke. 2021. ‘Crypto-Colonialists Use the Most Vulnerable People in the World as Guinea Pigs’. VICE Media.

|

||||

|

|

@ -1,18 +1,22 @@

|

|||

# Is crypto providing faster payment rails or better remittance services?

|

||||

# Crypto is not providing faster payment rails or better remittance services

|

||||

Since crypto assets [cannot function as a currency](is-bitcoin-currency.md) they are not useful in building payment rails or remittance services. Crypto assets can be used as an intermediate asset in which trades can be settled in, but this does not serve a technical of financial purpose and simply introduces an unnecessary conversion step for no reason.

|

||||

|

||||

If a person wants to send money abroad, say from US dollars to Indian rupees they would typically use a service like MoneyGram or WesternUnion. These services charge a transaction fee and do a direct swap of dollars to rupees from the reserves the company holds in both currencies.

|

||||

|

||||

If one postulates using a crypto asset or stablecoin as a means to do remittances then they are stilled faced with the *last leg problem*. Their relative in India still has to convert the crypto asset into the local currency to buy domestic goods and services since supermakets and stores don't accept crypto assets. So instead of a dollar-to-ruppee conversion we would hypothetically do a dollar-to-bitcoin-to-rupee conversion. This introduces [price-risk](../concepts/price-risk.md), [counterparty-risk](../concepts/counterparty-risk.md) and unnecessary conversion fees to accommodate the extraneous third exchange. This is unnecessary complexity and likely more expensive, for no reason.

|

||||

|

||||

See industry analysts describe this proble in more depth: [Does Bitcoin/Blockchain make sense for international money transfers?](https://www.saveonsend.com/bitcoin-blockchain-money-transfer/)

|

||||

|

||||

## References

|

||||

1. Cembalest, Michael. 2022. ‘The Maltese Falcoin: On Cryptocurrencies and Blockchains’.

|

||||

1. Rosenthal, David. n.d. ‘Stanford Lecture on Cryptocurrency’. Accessed 2 March 2022. https://blog.dshr.org/2022/02/ee380-talk.html.

|

||||

1. Steele, Graham. 2021. ‘The Miner of Last Resort: Digital Currency, Shadow Money and the Role of the Central Bank’. Technology and Government, Emerald Studies in Media and Communications, Forthcoming.

|

||||

1. Amato, Massimo, and Luca Fantacci. 2020. A Fistful of Bitcoins: The Risks and Opportunities of Virtual Currencies. Bocconi University Press. https://www.egeaeditore.it/ita/prodotti/economia/a-fistful-of-bitcoins.aspx.

|

||||

1. Coeckelbergh, Mark. 2015. Money Machines: Electronic Financial Technologies, Distancing and Responsibility in Global Finance. Routledge. https://doi.org/10.1177/0094306116671949n.

|

||||

1. Diehl, Stephen. 2021. ‘The Non-Innovation of Cryptocurrency’. 7 July 2021. https://www.stephendiehl.com/blog/non-innovation.html.

|

||||

1. Krugman, Paul. 2018. ‘Transaction Costs and Tethers: Why I’m a Crypto Skeptic’. The New York Times 21.

|

||||

1. ———. 2021. ‘Technobabble, Libertarian Derp and Bitcoin’. The New York Times 21.

|

||||

1. Plant, Luke. 2022. ‘The Technological Case against Bitcoin and Blockchain’. Luke Plant’s Home Page. 5 March 2022. https://lukeplant.me.uk/blog/posts/the-technological-case-against-bitcoin-and-blockchain/.

|

||||

1. Stinchcombe, Kai. 2017. ‘Ten Years In, Nobody Has Come Up With a Use for Blockchain’. Hackernoon. 22 December 2017. https://hackernoon.com/ten-years-in-nobody-has-come-up-with-a-use-case-for-blockchain-ee98c180100.

|

||||

1. Weaver, Nicholas. 2018. Blockchains and Cryptocurrencies: Burn It With Fire. Berkeley School of Information. https://www.youtube.com/watch?v=xCHab0dNnj4.

|

||||

1. White, Molly. 2022a. ‘Blockchain-Based Systems Are Not What They Say They Are’. Molly White (blog). 9 January 2022. https://blog.mollywhite.net/blockchains-are-not-what-they-say/.

|

||||

1. ———. 2022b. ‘Anonymous Cryptocurrency Wallets Are Not So Simple’. Molly White (blog). 12 February 2022. https://blog.mollywhite.net/anonymous-crypto-wallets/.

|

||||

1. ———. 2022c. ‘Cryptocurrency Off-Ramps, and the Shift towards Centralization’. Molly White. 12 February 2022. https://blog.mollywhite.net/off-ramps/.

|

||||

1. ———. 2022d. ‘Cryptocurrency’s Robinhood Effect’. Molly White. 17 February 2022. https://blog.mollywhite.net/cryptocurrencys-robinhood-effect/.

|

||||

1. Cembalest, Michael. 2022. ‘The Maltese Falcoin: On Cryptocurrencies and Blockchains’. https://privatebank.jpmorgan.com/content/dam/jpm-wm-aem/global/pb/en/insights/eye-on-the-market/the-maltese-falcoin.pdf.

|

||||

1. Weaver, Nicholas. 2018. Blockchains and Cryptocurrencies: Burn It With Fire. Berkeley School of Information. https://www.youtube.com/watch?v=xCHab0dNnj4.

|

||||

1. Steele, Graham. 2021. ‘The Miner of Last Resort: Digital Currency, Shadow Money and the Role of the Central Bank’. Technology and Government, Emerald Studies in Media and Communications, Forthcoming.

|

||||

1. Amato, Massimo, and Luca Fantacci. 2020. A Fistful of Bitcoins: The Risks and Opportunities of Virtual Currencies. Bocconi University Press. https://www.egeaeditore.it/ita/prodotti/economia/a-fistful-of-bitcoins.aspx.

|

||||

1. Krugman, Paul. 2018. ‘Transaction Costs and Tethers: Why I’m a Crypto Skeptic’. The New York Times 21.

|

||||

1. ———. 2021. ‘Technobabble, Libertarian Derp and Bitcoin’. The New York Times 21.

|

||||

1. Stinchcombe, Kai. 2017. ‘Ten Years In, Nobody Has Come Up With a Use for Blockchain’. Hackernoon. 22 December 2017. https://hackernoon.com/ten-years-in-nobody-has-come-up-with-a-use-case-for-blockchain-ee98c180100.

|

||||

|

|

@ -1,7 +1,7 @@

|

|||

# Bitcoin cannot function as a currency

|

||||

Unlike the namesake of "cryptocurrency" might imply, [bitcoin](../concepts/bitcoin.md) is not a [currency](../concepts/currency.md). It does not fulfil the economic definition of [money](../concepts/money.md). Instead bitcoin is best understood as a [speculative](../concepts/speculation.md) [cryptoasset](../concepts/cryptoasset.md) or [gambling](../concepts/gambling.md) product.

|

||||

|

||||

Since bitcoin is not issued by a sovereign state or [central-banks](../concepts/central-banks.md) there is no central party to manage the [deflationary](../concepts/deflationary.md) spirals that occur in the [price-formation](../concepts/price-formation.md) of the asset. Therefore it is subject to wild and uncontrollable volatility that makes it unsuitable as a *means of exchange*. No amount of technology can fix the volatility problem as it is a function of the economic design of the asset and its fixed supply. This arises out of the political imaginaries of the [neo-metallism](../notes/neo-metallism.md) school and [austrian-economics](../concepts/ideologies/austrian-economics.md) that informed the design of the bitcoin to resemble the historical [gold-standard](../concepts/gold-standard.md) and the conception of heterodox ideas of [sound-money](../concepts/sound-money.md).

|

||||

Since bitcoin is not issued by a sovereign state or [central-banks](../concepts/central-banks.md) there is no central party to manage the [deflationary](../concepts/deflationary.md) spirals that occur in the [price-formation](../concepts/price-formation.md) of the asset. Therefore it is subject to wild and uncontrollable volatility that makes it unsuitable as a *means of exchange*. No amount of technology can fix the volatility problem as it is a function of the economic design of the asset and its fixed supply. This arises out of the political imaginaries of the [neo-metallism](../notes/neo-metallism.md) school and [Austrian economics](../concepts/austrian-economics.md) that informed the design of the bitcoin to resemble the historical [gold-standard](../concepts/gold-standard.md) and the conception of heterodox ideas of [sound money](../concepts/sound-money.md).

|

||||

|

||||

As evidenced by real world context there are very few businesses that are willing to transact in bitcoin because of the price volatility. Companies that attempt to do this, such as Tesla, effectively issue an [option](../concepts/derivative.md) in which the goods or services payed are quoted at a strike price and if the transaction is reversed or goods returned the amount will be returned to the customer in a different currency at the strike price. This terms commerce into a [security](../concepts/security.md) transaction and is a taxable event.

|

||||

|

||||

|

|

@ -17,6 +17,7 @@ Since bitcoin is [deflationary](../concepts/deflationary.md) it encourages hordi

|

|||

1. Diehl, Stephen. 2021a. ‘The Non-Innovation of Cryptocurrency’. 7 July 2021. https://www.stephendiehl.com/blog/non-innovation.html.

|

||||

1. ———. 2021b. ‘The Intellectual Incoherence of Cryptoassets’. 7 November 2021. https://www.stephendiehl.com/blog/crypto-absurd.html.

|

||||

1. ———. n.d. ‘The Case Against Crypto’. Accessed 17 February 2022. https://www.stephendiehl.com/blog/against-crypto.html.

|

||||

1. Eich, Stefan. 2018. ‘The Currency of Politics’. The Political Theory of Money from Aristotle to Keynes.

|

||||

1. Gerard, David. 2017. Attack of the 50 Foot Blockchain: Bitcoin, Blockchain, Ethereum & Smart Contracts. David Gerard.

|

||||

1. Kolchinski, Alex. 2022. ‘Crypto Is an Unproductive Bubble’. Alex Kolchinski (blog). 18 March 2022. https://alexkolchinski.com/2022/03/18/crypto-is-an-unproductive-bubble/.

|

||||

1. Krugman, Paul. 2018. ‘Bitcoin Is Basically a Ponzi Scheme’. The Seattle Times 30.

|

||||

|

|

@ -26,12 +27,4 @@ Since bitcoin is [deflationary](../concepts/deflationary.md) it encourages hordi

|

|||

1. Plant, Luke. 2022. ‘The Technological Case against Bitcoin and Blockchain’. Luke Plant’s Home Page. 5 March 2022. https://lukeplant.me.uk/blog/posts/the-technological-case-against-bitcoin-and-blockchain/.

|

||||

1. Stinchcombe, Kai. 2018. ‘Blockchain Is Not Only Crappy Technology but a Bad Vision for the Future’. Medium (blog). 9 April 2018. https://medium.com/@kaistinchcombe/decentralized-and-trustless-crypto-paradise-is-actually-a-medieval-hellhole-c1ca122efdec.

|

||||

1. White, Molly. 2022a. ‘Cryptocurrency Off-Ramps, and the Shift towards Centralization’. Molly White. 12 February 2022. https://blog.mollywhite.net/off-ramps/.

|

||||

1. ———. 2022b. ‘Cryptocurrency’s Robinhood Effect’. Molly White. 17 February 2022. https://blog.mollywhite.net/cryptocurrencys-robinhood-effect/.

|

||||

|

||||

## References

|

||||

* [@taleb_bitcoin_2021-1]

|

||||

* [@corradi_disenchantment_2018]

|

||||

* [@nabilou_ignorance_2019]

|

||||

* [@krugman_brutal_2021]

|

||||

* [@krugman_technobabble_2021]

|

||||

* [@varoufakis_what_2021]

|

||||

1. ———. 2022b. ‘Cryptocurrency’s Robinhood Effect’. Molly White. 17 February 2022. https://blog.mollywhite.net/cryptocurrencys-robinhood-effect/.

|

||||

|

|

@ -5,13 +5,13 @@ Bitcoin is not compatible with ESG investing.

|

|||

|

||||

**Environmental Problems**

|

||||

|

||||

* [Environmental footprint of mining](environmental-footprint.md)

|

||||

* [Environmental footprint of mining](is-environmental-footprint.md)

|

||||

|

||||

**Sustainability Problems**

|

||||

**Social Problems**

|

||||

|

||||

* [Crypto is a market bubble](is-bubble.md)

|

||||

* [Predatory inclusion](is-predatory.md)

|

||||

* [Consumer protections](consumer-protections.md)

|

||||

* [Consumer protections](is-consumer-protections.md)

|

||||

* [Bitcoin is not a currency](is-bitcoin-currency.md)

|

||||

* [Private money is not sustainable](is-private-money.md)

|

||||

* [Crypto is not build a new financial system](is-new-financial-system.md)

|

||||

|

|

@ -26,7 +26,6 @@ Bitcoin is not compatible with ESG investing.

|

|||

* [Market manipulation](../concepts/market-manipulation.md)

|

||||

|

||||

## References

|

||||

|

||||

1. Gallersdörfer, Ulrich, Lena Klaaßen, and Christian Stoll. ‘Accounting for Carbon Emissions Caused by Cryptocurrency and Token Systems’, 2021. https://arxiv.org/abs/2111.06477.

|

||||

1. Goodkind, Andrew L., Benjamin A. Jones, and Robert P. Berrens. ‘Cryptodamages: Monetary Value Estimates of the Air Pollution and Human Health Impacts of Cryptocurrency Mining’. Energy Research and Social Science 59, no. March 2019 (2020): 101281. https://doi.org/10.1016/j.erss.2019.101281.

|

||||

1. Gallersdörfer, Ulrich, Lena Klaaßen, and Christian Stoll. ‘Accounting for Carbon Emissions Caused by Cryptocurrency and Token Systems’, 2021. https://arxiv.org/abs/2111.06477.

|

||||

|

|

@ -36,4 +35,5 @@ Bitcoin is not compatible with ESG investing.

|

|||

1. Schinckus, Christophe. ‘The Good, the Bad and the Ugly: An Overview of the Sustainability of Blockchain Technology’. Energy Research and Social Science 69, no. May (2020): 101614. https://doi.org/10.1016/j.erss.2020.101614.

|

||||

1. Vries, Alex De. ‘Bitcoin’s Energy Consumption Is Underestimated : A Market Dynamics Approach’. Energy Research & Social Science 70, no. July (2020): 101721. https://doi.org/10.1016/j.erss.2020.101721.

|

||||

1. Vries, Alex de. ‘Bitcoin’s Growing Energy Problem’. Joule 2, no. 5 (2018): 801–5. https://doi.org/10.1016/j.joule.2018.04.016.

|

||||

1. Vries, Alex de, and Christian Stoll. ‘Bitcoin’s Growing e-Waste Problem’. Resources, Conservation and Recycling 175, no. September (2021): 105901. https://doi.org/10.1016/j.resconrec.2021.105901.

|

||||

1. Vries, Alex de, and Christian Stoll. ‘Bitcoin’s Growing e-Waste Problem’. Resources, Conservation and Recycling 175, no. September (2021): 105901. https://doi.org/10.1016/j.resconrec.2021.105901.

|

||||

1. Wanat, Emanuel. 2021. ‘Are Crypto-Assets Green Enough? – An Analysis of Draft EU Regulation on Markets in Crypto Assets from the Perspective of the European Green Deal’. Osteuropa Recht 67 (2): 237–50. https://doi.org/10.5771/0030-6444-2021-2-237.

|

||||

|

|

@ -5,20 +5,20 @@ The technical purpose of blockchains is to create [censorship resistent](../conc

|

|||

|

||||

## References

|

||||

1. Schneier, Bruce. 2019. ‘There’s No Good Reason to Trust Blockchain Technology’. Wired Magazine. https://www.wired.com/story/theres-no-good-reason-to-trust-blockchain-technology/.

|

||||

1. Jeffries, Adrianne. 2018. ‘Blockchain Is Meaningless’. The Verge 7: 2018.

|

||||

1. Rosenthal, David. n.d. ‘Stanford Lecture on Cryptocurrency’. Accessed 2 March 2022. https://blog.dshr.org/2022/02/ee380-talk.html.

|

||||

1. Jeffries, Adrianne. 2018. ‘Blockchain Is Meaningless’. The Verge 7: 2018. https://www.theverge.com/2018/3/7/17091766/blockchain-bitcoin-ethereum-cryptocurrency-meaning.

|

||||

1. Stinchcombe, Kai. 2017. ‘Ten Years In, Nobody Has Come Up With a Use for Blockchain’. Hackernoon. 22 December 2017. https://hackernoon.com/ten-years-in-nobody-has-come-up-with-a-use-case-for-blockchain-ee98c180100.

|

||||

1. ———. 2018. ‘Blockchain Is Not Only Crappy Technology but a Bad Vision for the Future’. Medium (blog). 9 April 2018. https://medium.com/@kaistinchcombe/decentralized-and-trustless-crypto-paradise-is-actually-a-medieval-hellhole-c1ca122efdec.

|

||||

1. Orlowski, A. 2018. ‘Blockchain Study Finds 0.00% Success Rate and Vendors Don’t Call Back When Asked for Evidence’. The Register.

|

||||

1. Diehl, Stephen. 2021. ‘Blockchainism’. 11 December 2021. https://www.stephendiehl.com/blog/blockchainism.html.

|

||||

1. Pollock, Rufus. 2016. ‘Reflections on the Blockchain · Rufus Pollock Online’. 2 July 2016. https://rufuspollock.com/2016/07/02/reflections-on-the-blockchain/.

|

||||

1. Orlowski, A. 2018. ‘Blockchain Study Finds 0.00% Success Rate and Vendors Don’t Call Back When Asked for Evidence’. The Register. https://www.theregister.com/2018/11/30/blockchain_study_finds_0_per_cent_success_rate/.

|

||||

1. Manski, Sarah, and Michel Bauwens. 2020. ‘Reimagining New Socio-Technical Economics Through the Application of Distributed Ledger Technologies’. Frontiers in Blockchain 2 (January): 1–17. https://doi.org/10.3389/fbloc.2019.00029.

|

||||

1. Pardo-Guerra, Juan Pablo. 2019. Automating Finance. https://doi.org/10.1017/9781108677585.

|

||||

1. Rauchs, Michel, Apolline Blandin, Keith Bear, and Stephen B McKeon. 2019. ‘2nd Global Enterprise Blockchain Benchmarking Study’. http://ssrn.com/paper=3461765.

|

||||

1. Diehl, Stephen. 2021. ‘Blockchainism’. 11 December 2021. https://www.stephendiehl.com/blog/blockchainism.html.

|

||||

1. Diehl, Stephen. 2021a. ‘The Non-Innovation of Cryptocurrency’. 7 July 2021. https://www.stephendiehl.com/blog/non-innovation.html.

|

||||

———. 2021b. ‘The Handwavy Technobabble Nothingburger’. 24 November 2021. https://www.stephendiehl.com/blog/nothing-burger.html.

|

||||

1. Plant, Luke. 2022. ‘The Technological Case against Bitcoin and Blockchain’. Luke Plant’s Home Page. 5 March 2022. https://lukeplant.me.uk/blog/posts/the-technological-case-against-bitcoin-and-blockchain/.

|

||||

1. Weaver, Nicholas. 2018. Blockchains and Cryptocurrencies: Burn It With Fire. Berkeley School of Information. https://www.youtube.com/watch?v=xCHab0dNnj4.

|

||||

1. White, Molly. 2022a. ‘Blockchain-Based Systems Are Not What They Say They Are’. Molly White (blog). 9 January 2022. https://blog.mollywhite.net/blockchains-are-not-what-they-say/.

|

||||

1. ———. 2022b. ‘It’s Not Still the Early Days’. Molly White. 14 January 2022. https://blog.mollywhite.net/its-not-still-the-early-days/.

|

||||

1. Pollock, Rufus. 2016. ‘Reflections on the Blockchain · Rufus Pollock Online’. 2 July 2016. https://rufuspollock.com/2016/07/02/reflections-on-the-blockchain/.

|

||||

1. Bindseil, Ulrich, Patrick Papsdorf, and Jürgen Schaaf. 2022. ‘The Encrypted Threat: Bitcoin’s Social Cost and Regulatory Responses’. 7 January 2022. https://web.archive.org/web/20220107084533/https://www.suerf.org/docx/f_88b3febc5798a734026c82c1012408f5_38771_suerf.pdf.

|

||||

1. Bindseil, Ulrich, Patrick Papsdorf, and Jürgen Schaaf. 2022. ‘The Encrypted Threat: Bitcoin’s Social Cost and Regulatory Responses’. 7 January 2022. https://www.suerf.org/docx/f_88b3febc5798a734026c82c1012408f5_38771_suerf.pdf.

|

||||

|

|

@ -24,7 +24,6 @@ And several notable investors have also described it as a bubble:

|

|||

* George Soros

|

||||

|

||||

## References

|

||||

|

||||

1. Chancellor, Edward. 1999. ‘Devil Take the Hindmost: A History of Financial Speculation’.

|

||||

1. Blanchard, Olivier J, and Mark W Watson. 1982. ‘Bubbles, Rational Expectations and Financial Markets’. NBER Working Paper, no. w0945.

|

||||

1. Bernstein, William J. 2021. The Delusions of Crowds: Why People Go Mad in Groups. Grove Press.

|

||||

|

|

@ -34,9 +33,5 @@ And several notable investors have also described it as a bubble:

|

|||

1. Mackay, Charles. 2012. Extraordinary Popular Delusions and the Madness of Crowds. Simon and Schuster.

|

||||

1. Nabilou, Hossein, and André Prüm. 2019. ‘Ignorance, Debt, and Cryptocurrencies: The Old and the New in the Law and Economics of Concurrent Currencies’. Journal of Financial Regulation 5 (1): 29–63. https://doi.org/10.1093/jfr/fjz002.

|

||||

1. Smales, L. A. 2022. ‘Investor Attention in Cryptocurrency Markets’. International Review of Financial Analysis 79: 101972. https://doi.org/10.1016/j.irfa.2021.101972.

|

||||

|

||||

## References

|

||||

* [@blanchard_bubbles_1982]

|

||||

* [@caferra_bitcoin_2021]

|

||||

* [@fry_negative_2016]

|

||||

* [@tonelli_internet_2022]

|

||||

1. Kolchinski, Alex. 2022. ‘Crypto Is an Unproductive Bubble’. Alex Kolchinski (blog). 18 March 2022. https://alexkolchinski.com/2022/03/18/crypto-is-an-unproductive-bubble/.

|

||||

1. Krugman, Paul. 2021. ‘The Brutal Truth About Bitcoin’. The New York Times 21.

|

||||

|

|

@ -1,3 +1,16 @@

|

|||

# Are crypto tokens a means to accelerate the collapse of capitalism?

|

||||

# Crypto tokens are not a means to destroy capitalism

|

||||

|

||||

## References

|

||||

Crypto tokens are indeed a form of [predatory investment](../concepts/predatory-inclusion.md) that may have wide-reaching consequences in the lives of people it harms. However it is not a means to accelerate the collapse of capitalism even if one subscribes to the [accelerationism](../concepts/accelerationism.md) school of thought and believed this the acceleration of capitalism and its destruction was a good thing.

|

||||

|

||||

The crypto ideology is an extension of neoliberal project that aims to expand the scope and reach of markets to all aspects of human life, a concept often referred to [as hyperfinancialization](is-hyperfinancialization.md). Since crypto tokens aim to expand the scope of capitalism, they cannot bring about anything but more capitalism.

|

||||

|

||||

## References

|

||||

1. Reijers, Wessel, and Mark Coeckelbergh. 2018. ‘The Blockchain as a Narrative Technology: Investigating the Social Ontology and Normative Configurations of Cryptocurrencies’. Philosophy and Technology 31 (1): 103–30. https://doi.org/10.1007/s13347-016-0239-x.

|

||||

1. Golumbia, David. 2013a. ‘Cyberlibertarianism: The Extremist Foundations of “Digital Freedom.”’ Clemson University Department of English.

|

||||

1. ———. 2015. ‘Bitcoin as Politics: Distributed Right-Wing Extremism’. MoneyLab Reader: An Intervention in Digital Economy, Amsterdam: Institute of Network Cultures.

|

||||

1. Stinchcombe, Kai. 2018. ‘Blockchain Is Not Only Crappy Technology but a Bad Vision for the Future’. Medium (blog). 9 April 2018. https://medium.com/@kaistinchcombe/decentralized-and-trustless-crypto-paradise-is-actually-a-medieval-hellhole-c1ca122efdec.

|

||||

1. Brody, Ann, and Stéphane Couture. 2021. ‘Ideologies and Imaginaries in Blockchain Communities: The Case of Ethereum’. Canadian Journal of Communication 46 (3). https://doi.org/10.22230/cjc.2021v46n3a3701.

|

||||

1. DuPont, Quinn. 2016. ‘The Politics of Cryptography: Bitcoin and the Ordering Machines’. Journal of Peer Production 1 (4): 1–23. http://peerproduction.net/wp-content/uploads/2014/04/DuPont_draft_submission.pdf.

|

||||

1. Hellegren, Z. Isadora. 2017. ‘A History of Crypto-Discourse: Encryption as a Site of Struggles to Define Internet Freedom’. Internet Histories 1 (4): 285–311. https://doi.org/10.1080/24701475.2017.1387466.

|

||||

1. Jarvis, Craig. 2021. ‘Cypherpunk Ideology: Objectives, Profiles, and Influences (1992–1998)’. Internet Histories, 1–27. https://doi.org/10.1080/24701475.2021.1935547.

|

||||

1. Husain, Syed Omer, Alex Franklin, and Dirk Roep. 2020. ‘The Political Imaginaries of Blockchain Projects: Discerning the Expressions of an Emerging Ecosystem’. Sustainability Science, 1–16.

|

||||

|

|

@ -1,5 +1,5 @@

|

|||

# Crypto is not a solution for the unbanked

|

||||

Crypto is not a solution to unbanked, because by its [deflationary](../concepts/deflationary.md) design it [cannot function as a currency](is-bitcoin-currency.md) therefore it is unusable as a scaleable means for purchasing goods and services.

|

||||

Crypto is not a solution for the [unbanked](../concepts/unbanked.md), because by its [deflationary](../concepts/deflationary.md) design it [cannot function as a currency](is-bitcoin-currency.md) therefore it is unusable as a scaleable means for purchasing goods and services.

|

||||

|

||||

The purpose of retail banking services is to provide stable, reliable and safe means for citizens to transact with money that is safely custodied by a trusted third party with the guarantees of regulation by the government that the party will hold their accounts on their behalf. This includes practices like customer service, deposit insurance, fraud detection, transaction reversal and issuing of payment cards.

|

||||

|

||||

|

|

@ -16,8 +16,4 @@ The purpose of retail banking services is to provide stable, reliable and safe m

|

|||

1. Kapsis, I. (2021). Should we trade market stability for more financial inclusion? The case of crypto-assets regulation in EU. FinTech, Artificial Intelligence and the Law: Regulation and Crime Prevention, 85–104. https://doi.org/10.4324/9781003020998-9

|

||||

1. Sen, A., Lindquist, J., & Kolling, M. (2020). Who’s Cashing in? Contemporary Perspectives on New Monies and Global Cashlessness (Vol. 19). Berghahn Books.

|

||||

1. Swartz, L. (2020). New money: How payment became social media. Yale University Press. https://yalebooks.yale.edu/book/9780300233223/new-money

|

||||

1. Vasudevan, R. (2020). Libra and Facebook’s Money Illusion. Challenge, 63(1), 21–39. https://doi.org/10.1080/05775132.2019.1684662

|

||||

|

||||

## References

|

||||

* [@koning_bitcoin_2020]

|

||||

* [@knauer_what_2019]

|

||||

1. Vasudevan, R. (2020). Libra and Facebook’s Money Illusion. Challenge, 63(1), 21–39. https://doi.org/10.1080/05775132.2019.1684662

|

||||

|

|

@ -1,5 +1,5 @@

|

|||

# Bitcoin is the basis for a new gold standard

|

||||

The neo-metallist claim is that bitcoin can operate as a new asset class which exhibits similar financial properties to [gold](../concepts/gold.md). The strong version of this claim asserts that a new [gold-standard](../concepts/gold-standard.md) can be built on top of bitcoin and that this can form the basis for a market economy.

|

||||

# Bitcoin is not the basis for a new gold standard

|

||||

The neo-metallist claim is that bitcoin can operate as a new asset class which exhibits similar financial properties to [gold](../concepts/gold.md). The strong version of this claim asserts that a new [gold standard](../concepts/gold-standard.md) can be built on top of bitcoin and that this can form the basis for a market economy.

|

||||

|

||||

These claims do not stand up to scrutiny as bitcoin has no consistent track record of being a reliable store of value, it's price movements are extremely volatile and thus is not a reliable place to store value on long time scales. Bitcoin's price behavior is uncorrelated with gold and is largely correlated with the broader stock market making it an unreliable safe haven in times of market volatility since it is directly exposed to the price action of the Nasdaq.

|

||||

|

||||

|

|

@ -8,19 +8,10 @@ Bitcoin has no historical track record of being a store of value and lacks the m

|

|||

Even if bitcoin could function as a new gold standard. The [gold-standard](../concepts/gold-standard.md) and the notion of [sound-money](../concepts/sound-money.md) are undesirable foundations for a [currency](../concepts/currency.md) and were subject to extreme shocks and deflationary spirals, and as such were abandoned in the mid 20th century in favour of the [central-banks](../concepts/central-banks.md) and fiat monetary system.

|

||||

|

||||

## References

|

||||

|

||||

1. Cembalest, M. (2022). The Maltese Falcoin: On Cryptocurrencies and Blockchains (p. 31).

|

||||

1. Allon, F. (2018). Money after Blockchain: Gold, Decentralised Politics and the New Libertarianism. Australian Feminist Studies, 33(96), 223–243. https://doi.org/10.1080/08164649.2018.1517245

|

||||

1. Bernanke, B. S. (2004). Essays on the Great Depression. Princeton University Press.

|

||||

1. Caferra, R., Tedeschi, G., & Morone, A. (2021). Bitcoin: Bubble that bursts or Gold that glitters? Economics Letters, 205, 109942. https://doi.org/10.1016/j.econlet.2021.109942

|

||||

1. Doctorow, C. (2022, February 3). Pluralistic: 03 Feb 2022 – Pluralistic: Daily links from Cory Doctorow. https://pluralistic.net/2022/02/03/liquidation-preference/

|

||||

1. Selmi, R., Bouoiyour, J., & Wohar, M. E. (2022). “Digital Gold” and geopolitics. Research in International Business and Finance, 59, 101512. https://doi.org/10.1016/j.ribaf.2021.101512

|

||||

1. Wang, G., Tang, Y., Xie, C., & Chen, S. (2019). Is bitcoin a safe haven or a hedging asset? Evidence from China. Journal of Management Science and Engineering, 4(3), 173–188. https://doi.org/10.1016/j.jmse.2019.09.001

|

||||

|

||||

## References

|

||||

* [@cembalest_maltese_2022]

|

||||

* [@taleb_bitcoin_2021]

|

||||

* [@caferra_bitcoin_2021]

|

||||

* [@weisenthal_bitcoin_nodate]

|

||||

* [@krugman_bitcoin_2018]

|

||||

* [@bernanke_essays_2004]

|

||||

1. Cembalest, M. (2022). The Maltese Falcoin: On Cryptocurrencies and Blockchains (p. 31).

|

||||

1. Wang, G., Tang, Y., Xie, C., & Chen, S. (2019). Is bitcoin a safe haven or a hedging asset? Evidence from China. Journal of Management Science and Engineering, 4(3), 173–188. https://doi.org/10.1016/j.jmse.2019.09.001

|

||||

|

|

@ -1,3 +1,19 @@

|

|||

# Is web3 a means to dismantle the American tech hegemony?

|

||||

|

||||

## References

|

||||

Web3 is not a means to disrupt the American tech hegemony, companies like Google, Facebook, Amazon etc. Since web3 has no coherent meaning or purpose, all projects that are currently being developed under the web3 umbrella are aimless technical Potemkin villages that mask thinly veiled [pump and dump](../concepts/pump-and-dump.md) schemes based on [securities](../concepts/security.md) [regulatory arbitrage](../concepts/regulatory-arbitrage.md). This type of company structure is not set up for long term growth or product delivery outside of pumping more token schemes.

|

||||

|

||||

This is further evidenced by the simple fact that [blockchain](../concepts/blockchain.md) technologies have intractable scalability problems, and that the only means they do scale is by [recentralization](../concepts/recentralization.md) thereby recreating just another corporate monolith but based on inferior technology and without the ability to perform [regulatory arbitrage](../concepts/regulatory-arbitrage.md)..

|

||||

|

||||

There is no future in web3 that poses any threat to tech monopoly because there simply is no meaningful tech to challenge any real business model.

|

||||

|

||||

## References

|

||||

1. Marx, Paris. n.d. ‘Why Web3, the Blockchain and Crypto Internet, Is Doomed to Fail’. Accessed 29 March 2022. https://www.businessinsider.com/web3-blockchain-crypto-internet-doomed-fail-doesnt-live-up-hype-2022-3?r=US&IR=T.

|

||||

1. Morozov, Evgeny. 2022. ‘Web3: A Map in Search of Territory’. The Crypto Syllabus. 13 January 2022. https://the-crypto-syllabus.com/web3-a-map-in-search-of-territory/.

|

||||

1. O’Reilly, Tim. 2021. ‘Why It’s Too Early to Get Excited About Web3’. O’Reilly Media. 13 December 2021. https://www.oreilly.com/radar/why-its-too-early-to-get-excited-about-web3/.

|

||||

1. Weaver, Nicholas. 2021. ‘The Web3 Fraud’. USENIX. 16 December 2021. https://www.usenix.org/publications/loginonline/web3-fraud.

|

||||

1. Tante. 2021. ‘The Third Web’. Nodes in a Social Network (blog). 17 December 2021. https://tante.cc/2021/12/17/the-third-web/.

|

||||

1. Levine, Matt. 2022. ‘Web3 Takes Trust Too’. 10 January 2022. https://www.bloomberg.com/opinion/articles/2022-01-10/web3-takes-trust-too.

|

||||

1. Soatok. 2021. ‘Against Web3 and Faux-Decentralization’. Dhole Moments. 19 October 2021. https://soatok.blog/2021/10/19/against-web3-and-faux-decentralization/.

|

||||

1. Zitron, Ed. 2022. ‘Solutions That Create Problems’. Substack newsletter. Ed Zitron’s Where’s Your Ed At (blog). 23 February 2022. https://ez.substack.com/p/solutions-that-create-problems.

|

||||

1. Diehl, Stephen. 2021. ‘Web3 Is Bullshit’. 4 December 2021. https://www.stephendiehl.com/blog/web3-bullshit.html.

|

||||

1. White, Molly. 2022. ‘It’s Not Still the Early Days’. Molly White. 14 January 2022. https://blog.mollywhite.net/its-not-still-the-early-days/.

|

||||

|

|

@ -3,9 +3,9 @@ Bitcoin [mining](../concepts/mining.md) is enormously harmful to the environment

|

|||

|

||||

1. E-waste from discarded or broken ASIC mining equipment, graphics cards and servers.

|

||||

2. Carbon release from fossil fuels used to power mining data centres

|

||||

3. Opportunity cost of the energy used to run [consensus algorithm](../concepts/consensus-algorithm.md) compared to more efficient of efficient [real time gross settlement systems](../concepts/rtgs.md) and traditional [payment rails](transnational-payment.md) such as SWIFT, SEPA, Visa and ACH.

|

||||

3. Opportunity cost of the energy used to run [consensus algorithm](../concepts/consensus-algorithm.md) compared to more efficient of efficient [real time gross settlement systems](../concepts/rtgs.md) and traditional [payment rails](is-transnational-payment.md) such as SWIFT, SEPA, Visa and ACH.

|

||||

|

||||

Crypto assets are not [providing access to the unbanked](crypto-unbanked.md) and cannot fulfil even a tiny fraction of the services provided by the global banking sector. Crypto assets like [bitcoin](../concepts/bitcoin.md) are simply a very inefficient and settlement to issue a speculative [cryptoasset](../concepts/cryptoasset.md) used primarily for [gambling](../concepts/gambling.md) and [illicit financing](../concepts/illicit-financing.md).

|

||||

Crypto assets are not [providing access to the unbanked](is-crypto-unbanked.md) and cannot fulfil even a tiny fraction of the services provided by the global banking sector. Crypto assets like [bitcoin](../concepts/bitcoin.md) are simply a very inefficient and settlement to issue a speculative [cryptoasset](../concepts/cryptoasset.md) used primarily for [gambling](../concepts/gambling.md) and [illicit financing](../concepts/illicit-financing.md).

|

||||

|

||||

BItcoin mining has the equivalent power consumption of the state of Argentina, a country with a population of 45 million people. Bitcoin mining has an e-waste footprint comparable to that of entire population of Germany.

|

||||

|

||||

|

|

@ -22,11 +22,4 @@ Crypto assets are not gambling if one participates in a [cartel](../concepts/car

|

|||

1. ———. 2018b. ‘Transaction Costs and Tethers: Why I’m a Crypto Skeptic’. The New York Times 21.

|

||||

1. ———. 2021. ‘The Brutal Truth About Bitcoin’. The New York Times 21.

|

||||

1. Taleb, Nassim Nicholas. 2021. ‘Bitcoin, Currencies, and Fragility’. ArXiv:2106.14204 [Physics, q-Fin], July. http://arxiv.org/abs/2106.14204.

|

||||

1. Weaver, Nicholas. 2018. Blockchains and Cryptocurrencies: Burn It With Fire. Berkeley School of Information. https://www.youtube.com/watch?v=xCHab0dNnj4.

|

||||

|

||||

## References

|

||||

* [@knauer_what_2019]

|

||||

* [@barrett_why_2021]

|

||||

* [@powell_crypto-shills_2019]

|

||||

* [@panos_financial_2019]

|

||||

* [@koning_bitcoin_2020]

|

||||

1. Weaver, Nicholas. 2018. Blockchains and Cryptocurrencies: Burn It With Fire. Berkeley School of Information. https://www.youtube.com/watch?v=xCHab0dNnj4.

|

||||

|

|

@ -0,0 +1,15 @@

|

|||

# Crypto assets are not a hedge against the "debasement" of the dollar

|

||||

Crypto assets are not a hedge against the "debasement" of the dollar. This thesis is predicated on an [Austrian economics](../concepts/austrian-economics.md) reading of United States monetary policy and policy a conspiracy theories about the Federal Reserve.

|

||||

|

||||

As part of the normal functioning of the dollar system, the Federal Reserve will make

|

||||

[interventionist](../concepts/keynsian-economics.md) adjustments to its quantitative easing policy and interest rates with the aims of achieving dollar price stability. The economy adjusts to these changes and factors them into the pricing of goods and services and this system results in relatively predictable inflation which encourages economic growth. The use of the pejorative term "debasement" to describe the natural and principled monetary policy rests on a fallacy which presumes fringe economic theories.

|

||||

|

||||

Crypto assets are not a hedge against these empty notions, because "debasement" does not exist as a phenomenon.

|

||||

|

||||

## References

|

||||

1. Hanley, Brian P. 2018. ‘The False Premises and Promises of Bitcoin’. ArXiv:1312.2048 [Cs, q-Fin], July. http://arxiv.org/abs/1312.2048.

|

||||

1. Roche, Cullen O. 2011. ‘Understanding the Modern Monetary System’. http://ssrn.com/paper=1905625.

|

||||

1. Binder, Carola. 2021. ‘Technopopulism and Central Banks’. SSRN Electronic Journal. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3823456.

|

||||

1. Braun, Benjamin, and Daniela Gabor. 2019. ‘Central Banking, Shadow Banking, and Infrastructural Power’. https://doi.org/10.31235/osf.io/nf9ms.

|

||||

1. Brennecke, Martin, Benjamin Schellinger, Nils Urbach, and Tobias Guggenberger. 2022. ‘The De-Central Bank in Decentralized Finance: A Case Study of MakerDAO’. In 55th Hawaii International Conference on System Sciences (2022). https://doi.org/10.24251/HICSS.2022.737.

|

||||

1. Malloy, Matthew, and David Lowe. 2021. ‘Global Stablecoins: Monetary Policy Implementation Considerations from the U.S. Perspective’. Finance and Economics Discussion Series 2021 (020): 1–14. https://doi.org/10.17016/feds.2021.020.

|

||||

|

|

@ -0,0 +1,15 @@

|

|||

# Are crypto assets a hedge against inflation?

|

||||

Since [crypto asset](../concepts/cryptoasset.md) have no exposure to domestic commodities there is no evidence of anti-correlation with a basket of goods that would be inversely to the national [currency](../concepts/currency.md) in times of inflation. Instead crypto assets seem largely correlated with the broader [stock](../concepts/stock.md) market and as such are not a hedge against any macroeconomic factors of either inflation or equity markets.

|

||||

|

||||

[Crypto assets](../concepts/cryptoasset.md) are also not a reliable [store of value](../concepts/store-of-value.md) in times of market instability, and as such do not provide a safe haven of any form since they are largely correlated with the broader market and exposed to the same shocks.

|

||||

|

||||

In his whitepaper *Bitcoin, Currencies, and Fragility*, Nassim Taleb deconstructs the "inflation hedge" thesis:

|

||||

|

||||

> The experience of March 2020, during the market panic upon the onset of the pandemic, when bitcoin dropped farther than the stock market —and subsequently recovered with it upon the massive injection of liquidity is sufficient evidence that it cannot remotely be used as a tail hedge against systemic risk. Furthermore, bitcoin appears to respond to liquidity, exactly like other bubble items. It is also uncertain what could happen should the internet experience a general, or an even a regional, outage — particularly if it takes place during a financial collapse.

|

||||

|

||||

## References

|

||||

1. Shaffer, Daniel S. 2010. Profiting in Economic Storms: A Historic Guide to Surviving Depression, Deflation, Hyperinflation, and Market Bubbles. John Wiley & Sons.

|

||||

1. Taleb, Nassim Nicholas. 2021. ‘Bitcoin, Currencies, and Fragility’. ArXiv:2106.14204 [Physics, q-Fin], July. http://arxiv.org/abs/2106.14204.

|

||||

1. Wang, Gangjin, Yanping Tang, Chi Xie, and Shou Chen. 2019. ‘Is Bitcoin a Safe Haven or a Hedging Asset? Evidence from China’. Journal of Management Science and Engineering 4 (3): 173–88. https://doi.org/10.1016/j.jmse.2019.09.001.

|

||||

1. Cembalest, Michael. 2022. ‘The Maltese Falcoin: On Cryptocurrencies and Blockchains’.

|

||||

1. Frisch, Helmut. 1983. Theories of Inflation. Cambridge University Press.

|

||||

|

|

@ -1,32 +1,40 @@

|

|||

# Is crypto bringing about the "financialization of everything"?

|

||||

|

||||

The purpose of NFTs and crypto projects generally is to further expand the scope [artificial scarcity](../concepts/artificial-scarcity.md), [enclose](../concepts/enclosure.md) and financialize greater portions of the human experience. The stated aim of the web3 and crypto project is world in which all aspects of human life (art, justice, philosophy, politics, relationships) are simply [ficticious commodities](../concepts/ficticious-commodity.md) to be traded in a market place and that human beings should subordinate all free will, individuality and rationality to the market.

|

||||

|

||||

The embodiment of the web3 and crypto ideology is an example of what the political theorist Macpherson denoted *possessive individualism*:

|

||||

|

||||

> [Possessive individualism is a philosophy] in which an individual is conceived as the sole proprietor of his or her skills and owes nothing to society for them. These skills (and those of others) are a commodity to be bought and sold on the open market, and in such a society is demonstrated a selfish and unending thirst for consumption which is considered the crucial core of human nature.

|

||||

|

||||

Projects like NFTs and the their increasing enclosure of culture have indicated that the intent of crypto is nothing but the complete domination of the human experience by Capital in the bleak dystopian future imagined by their acolytes.

|

||||

|

||||

## References

|

||||

* Bellinger, Matthew. 2018. ‘The Rhetoric of Bitcoin: Money, Politics, and the Construction of Blockchain Communities’. ResearchWorks Archive. PhD Thesis. https://digital.lib.washington.edu/researchworks/handle/1773/43342.

|

||||

* Breidbach, Christoph F., and Silviana Tana. 2021. ‘Betting on Bitcoin: How Social Collectives Shape Cryptocurrency Markets’. Journal of Business Research 122: 311–20. https://doi.org/10.1016/j.jbusres.2020.09.017.

|

||||

* Bruun, Maja Hojer, Astrid Oberborbeck Andersen, and Adrienne Mannov. 2020. ‘Infrastructures of Trust and Distrust: The Politics and Ethics of Emerging Cryptographic Technologies’. Anthropology Today 36 (2): 13–17. https://doi.org/10.1111/1467-8322.12562.

|

||||

* Diehl, Stephen. 2021a. ‘Gamestop, Bitcoin and the Commoditization of Populist Rage’. 3 February 2021. https://www.stephendiehl.com/blog/gamestop.html.

|

||||

* *———. n.d. ‘The Case Against Crypto’. Accessed 17 February 2022. https://www.stephendiehl.com/blog/against-crypto.html.

|

||||

* Lee, Seung Cheol. 2020. ‘Magical Capitalism, Gambler Subjects: South Korea’s Bitcoin Investment Frenzy’. Cultural Studies 0 (0): 1–24. https://doi.org/10.1080/09502386.2020.1788620.

|

||||

* Starita, G D. 2018. ‘On Bitcoin Usage, Techno-Optimism and Participation-An Anthropological Perspective on Rovereto s Bitcoin Valley Users’. Master’s Thesis. https://dspace.library.uu.nl/handle/1874/374186.

|

||||

* Stephenson, Will. n.d. ‘Cryptonomicon’. Harpers Review. Accessed 2 March 2022. https://harpers.org/archive/2022/03/cryptonomicon-bitcoin-maximalists-miami/.

|

||||

* Stinchcombe, Kai. 2018. ‘Blockchain Is Not Only Crappy Technology but a Bad Vision for the Future’. Medium (blog). 9 April 2018. https://medium.com/@kaistinchcombe/decentralized-and-trustless-crypto-paradise-is-actually-a-medieval-hellhole-c1ca122efdec.

|

||||

* Tante. 2021. ‘The Third Web’. Nodes in a Social Network (blog). 17 December 2021. https://tante.cc/2021/12/17/the-third-web/.

|

||||

* Warzel, Charlie. 2021. ‘The Absurdity Is the Point’. Substack newsletter. Galaxy Brain (blog). 11 May 2021. https://warzel.substack.com/p/the-absurdity-is-the-point.

|

||||

* Weisenthal, Joe. n.d. ‘Bitcoin Is a Faith-Based Asset’. Accessed 2 March 2022. https://www.bloomberg.com/news/articles/2021-01-21/bitcoin-is-a-faith-based-asset-joe-weisenthal.

|

||||

* Xu, Yizhou. 2021. ‘Digitizing Death: Commodification of Joss Paper on Chinese Online Cemetery’. Journal of Cultural Economy 0 (0): 1–17. https://doi.org/10.1080/17530350.2021.1952099.

|

||||

* Aharon, David Y., and Ender Demir. 2021. ‘NFTs and Asset Class Spillovers: Lessons from the Period around the COVID-19 Pandemic’. Finance Research Letters, 102515. https://doi.org/10.1016/j.frl.2021.102515.

|

||||

* Bodó, Balázs, Alexandra Giannopoulou, João Quintais, and Péter Mezei. 2022. ‘The Rise of NFTs: These Aren’t the Droids You’re Looking For’. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4000423.

|

||||

* Diehl, Stephen. 2021. ‘The Tinkerbell Griftopia’. 19 November 2021. https://www.stephendiehl.com/blog/tinkerbell.html.

|

||||

* Dowling, Michael. 2021. ‘Fertile LAND: Pricing Non-Fungible Tokens’. Finance Research Letters, 102096. https://doi.org/10.1016/j.frl.2021.102096.

|

||||

* Fairfield, Joshua. 2021. ‘Tokenized: The Law of Non-Fungible Tokens and Unique Digital Property’. Indiana Law Journal, 1–99. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3821102.

|

||||

* Frye, Brian L. 2021. ‘After Copyright: Pwning NFTs in a Clout Economy’. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3971240.

|

||||

* *———. n.d. ‘How to Sell NFTs Without Really Trying’. Harvard Journal of Sports and Entertainment Law, Forthcoming. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3930430.

|

||||

* Gibson, Johanna. 2021. ‘The Thousand-and-Second Tale of NFTS, as Foretold by Edgar Allan Poe’. Queen Mary Journal of Intellectual Property 11 (3): 249–69. https://doi.org/10.4337/qmjip.2021.03.00.

|

||||

* Guadamuz, Andres. 2021. ‘The Treachery of Images: Non-Fungible Tokens and Copyright’. SSRN Electronic Journal 16 (12): 1367–85. https://doi.org/10.2139/ssrn.3905452.

|

||||

* Kim, Soyeon. 2020. ‘Fractional Ownership, Democratization, and Bubble Formation - The Impact of Blockchain Enabled Asset Tokenization’. 26th Americas Conference on Information Systems, AMCIS 2020, 0–5. https://aisel.aisnet.org/amcis2020/adv_info_systems_research/adv_info_systems_research/19/.

|

||||

* Kong, De-Rong, and Tse-Chun Lin. 2021. ‘Alternative Investments in the Fintech Era: The Risk and Return of Non-Fungible Token (NFT)’. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3914085.

|

||||

* Low, Kelvin F K. 2021. ‘The Emperor’s New Art: Cryptomania, Art & Property’. Art & Property. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3978241.

|

||||

* Mackenzie, Simon, and Diāna Bērziņa. 2021. ‘NFTs: Digital Things and Their Criminal Lives’. Crime, Media, Culture, 17416590211039796. https://doi.org/10.1177/17416590211039797.

|

||||

* Nadini, Matthieu, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino, Luca Maria Aiello, and Andrea Baronchelli. 2021. ‘Mapping the NFT Revolution: Market Trends, Trade Networks, and Visual Features’. Scientific Reports 11 (1). https://doi.org/10.1038/s41598-021-00053-8.

|

||||

* *‘NFTs, Cryptocurrencies and Web3 Are Multilevel Marketing Schemes for a New Generation - WSJ’. n.d. Accessed 14 March 2022. https://www.wsj.com/articles/nfts-cryptocurrencies-and-web3-are-multilevel-marketing-schemes-for-a-new-generation-11645246824.

|

||||

* Olson, Dan. 2022a. Line Goes Up – The Problem With NFTs. https://www.youtube.com/watch?v=YQ_xWvX1n9g.

|

||||

1. Olson, Dan. 2022a. Line Goes Up – The Problem With NFTs. https://www.youtube.com/watch?v=YQ_xWvX1n9g.

|

||||

1. McKay, Ian (2014). "A Half-Century of Possessive Individualism: C.B. Macpherson and the Twenty-First-Century Prospects of Liberalism". Journal of the Canadian Historical Association. 25 (1): 307–340. doi:10.7202/1032806ar. ISSN 1712-6274.

|

||||

1. Bellinger, Matthew. 2018. ‘The Rhetoric of Bitcoin: Money, Politics, and the Construction of Blockchain Communities’. ResearchWorks Archive. PhD Thesis. https://digital.lib.washington.edu/researchworks/handle/1773/43342.

|

||||

1. Breidbach, Christoph F., and Silviana Tana. 2021. ‘Betting on Bitcoin: How Social Collectives Shape Cryptocurrency Markets’. Journal of Business Research 122: 311–20. https://doi.org/10.1016/j.jbusres.2020.09.017.

|

||||

1. Bruun, Maja Hojer, Astrid Oberborbeck Andersen, and Adrienne Mannov. 2020. ‘Infrastructures of Trust and Distrust: The Politics and Ethics of Emerging Cryptographic Technologies’. Anthropology Today 36 (2): 13–17. https://doi.org/10.1111/1467-8322.12562.

|

||||

1. Diehl, Stephen. 2021a. ‘Gamestop, Bitcoin and the Commoditization of Populist Rage’. 3 February 2021. https://www.stephendiehl.com/blog/gamestop.html.

|

||||

1. *———. n.d. ‘The Case Against Crypto’. Accessed 17 February 2022. https://www.stephendiehl.com/blog/against-crypto.html.

|

||||

1. Lee, Seung Cheol. 2020. ‘Magical Capitalism, Gambler Subjects: South Korea’s Bitcoin Investment Frenzy’. Cultural Studies 0 (0): 1–24. https://doi.org/10.1080/09502386.2020.1788620.

|

||||

1. Starita, G D. 2018. ‘On Bitcoin Usage, Techno-Optimism and Participation-An Anthropological Perspective on Rovereto s Bitcoin Valley Users’. Master’s Thesis. https://dspace.library.uu.nl/handle/1874/374186.

|

||||

1. Stephenson, Will. n.d. ‘Cryptonomicon’. Harpers Review. Accessed 2 March 2022. https://harpers.org/archive/2022/03/cryptonomicon-bitcoin-maximalists-miami/.

|

||||

1. Stinchcombe, Kai. 2018. ‘Blockchain Is Not Only Crappy Technology but a Bad Vision for the Future’. Medium (blog). 9 April 2018. https://medium.com/@kaistinchcombe/decentralized-and-trustless-crypto-paradise-is-actually-a-medieval-hellhole-c1ca122efdec.

|

||||

1. Tante. 2021. ‘The Third Web’. Nodes in a Social Network (blog). 17 December 2021. https://tante.cc/2021/12/17/the-third-web/.

|

||||

1. Warzel, Charlie. 2021. ‘The Absurdity Is the Point’. Substack newsletter. Galaxy Brain (blog). 11 May 2021. https://warzel.substack.com/p/the-absurdity-is-the-point.

|

||||

1. Weisenthal, Joe. n.d. ‘Bitcoin Is a Faith-Based Asset’. Accessed 2 March 2022. https://www.bloomberg.com/news/articles/2021-01-21/bitcoin-is-a-faith-based-asset-joe-weisenthal.

|

||||

1. Xu, Yizhou. 2021. ‘Digitizing Death: Commodification of Joss Paper on Chinese Online Cemetery’. Journal of Cultural Economy 0 (0): 1–17. https://doi.org/10.1080/17530350.2021.1952099.

|

||||

1. Aharon, David Y., and Ender Demir. 2021. ‘NFTs and Asset Class Spillovers: Lessons from the Period around the COVID-19 Pandemic’. Finance Research Letters, 102515. https://doi.org/10.1016/j.frl.2021.102515.

|

||||

1. Bodó, Balázs, Alexandra Giannopoulou, João Quintais, and Péter Mezei. 2022. ‘The Rise of NFTs: These Aren’t the Droids You’re Looking For’. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4000423.

|

||||

1. Diehl, Stephen. 2021. ‘The Tinkerbell Griftopia’. 19 November 2021. https://www.stephendiehl.com/blog/tinkerbell.html.

|

||||

1. Dowling, Michael. 2021. ‘Fertile LAND: Pricing Non-Fungible Tokens’. Finance Research Letters, 102096. https://doi.org/10.1016/j.frl.2021.102096.

|

||||

1. Fairfield, Joshua. 2021. ‘Tokenized: The Law of Non-Fungible Tokens and Unique Digital Property’. Indiana Law Journal, 1–99. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3821102.

|

||||

1. Frye, Brian L. 2021. ‘After Copyright: Pwning NFTs in a Clout Economy’. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3971240.

|

||||

1. *———. n.d. ‘How to Sell NFTs Without Really Trying’. Harvard Journal of Sports and Entertainment Law, Forthcoming. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3930430.

|

||||

1. Gibson, Johanna. 2021. ‘The Thousand-and-Second Tale of NFTS, as Foretold by Edgar Allan Poe’. Queen Mary Journal of Intellectual Property 11 (3): 249–69. https://doi.org/10.4337/qmjip.2021.03.00.

|

||||

1. Guadamuz, Andres. 2021. ‘The Treachery of Images: Non-Fungible Tokens and Copyright’. SSRN Electronic Journal 16 (12): 1367–85. https://doi.org/10.2139/ssrn.3905452.

|

||||

1. Kim, Soyeon. 2020. ‘Fractional Ownership, Democratization, and Bubble Formation - The Impact of Blockchain Enabled Asset Tokenization’. 26th Americas Conference on Information Systems, AMCIS 2020, 0–5. https://aisel.aisnet.org/amcis2020/adv_info_systems_research/adv_info_systems_research/19/.

|

||||

1. Kong, De-Rong, and Tse-Chun Lin. 2021. ‘Alternative Investments in the Fintech Era: The Risk and Return of Non-Fungible Token (NFT)’. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3914085.

|

||||

1. Low, Kelvin F K. 2021. ‘The Emperor’s New Art: Cryptomania, Art & Property’. Art & Property. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3978241.

|

||||

1. Mackenzie, Simon, and Diāna Bērziņa. 2021. ‘NFTs: Digital Things and Their Criminal Lives’. Crime, Media, Culture, 17416590211039796. https://doi.org/10.1177/17416590211039797.

|

||||

1. Nadini, Matthieu, Laura Alessandretti, Flavio Di Giacinto, Mauro Martino, Luca Maria Aiello, and Andrea Baronchelli. 2021. ‘Mapping the NFT Revolution: Market Trends, Trade Networks, and Visual Features’. Scientific Reports 11 (1). https://doi.org/10.1038/s41598-021-00053-8.

|

||||

|

|

@ -1,19 +1,17 @@

|

|||

# Legality of crypto assets

|

||||

Crypto assets are unlicensed [security](../concepts/security.md) contracts for unregulated [speculative](../concepts/speculation.md) investments. The legality of this depends on jurisdiction.

|

||||

|

||||

Crypto assets are unlicensed [security](../concepts/security.md) contracts for unregulated [speculative](../concepts/speculation.md) investments. Crypto assets are effectively like buying unregulated penny stocks, except with no recourse to the courts in the case of the project being a [Ponzi scheme](../concepts/ponzi-scheme.md) or [exit scam](../concepts/exit-scam.md).

|

||||

|

||||

The legality of buying these risky products depends on the jurisdiction of the buyer and seller.

|

||||

|

||||

In the United States the sale of unregistered securities to the public is illegal. The legality of the purchase of of unregistered securities will depend on the facts and circumstances of the sale, but regardless of legality these type of extra-legal transactions expose the buyer to unnecessary [risk](../concepts/risk.md) compared to buying normal [financial assets](../concepts/financial-asset.md) within the regulatory perimeter. Buying crypto assets is thus legally inadvisable from both a risk and compliance perspective.

|

||||

|

||||

## References

|

||||

1. Bindseil, Ulrich, Patrick Papsdorf, and Jü rgen Schaaf. 2022. ‘The Encrypted Threat: Bitcoin’s Social Cost and Regulatory Responses’.

|

||||

1. Diehl, Stephen. 2021a. ‘The Political Case for a Blanket Cryptocurrency Ban’. 30 March 2021. https://www.stephendiehl.com/blog/banbitcoin.html.

|

||||

———. 2021b. ‘How to Destroy Bitcoin’. 13 July 2021. https://www.stephendiehl.com/blog/destroy-bitcoin.html.

|

||||

1. Bindseil, Ulrich, Patrick Papsdorf, and Jürgen Schaaf. 2022. ‘The Encrypted Threat: Bitcoin’s Social Cost and Regulatory Responses’. 7 January 2022. https://www.suerf.org/docx/f_88b3febc5798a734026c82c1012408f5_38771_suerf.pdf.

|

||||

1. ‘Guidance on Cryptoassets’. 2019. Financial Conduct Authority. https://www.fca.org.uk/publication/consultation/cp19-03.pdf#page=11.

|

||||

1. Diehl, Stephen. 2021a. ‘The Political Case for a Blanket Cryptocurrency Ban’. 30 March 2021. https://www.stephendiehl.com/blog/banbitcoin.html.

|

||||

1. Hacker, Philipp, and Chris Thomale. 2018. ‘Crypto-Securities Regulation: ICOs, Token Sales and Cryptocurrencies under EU Financial Law’. European Company and Financial Law Review 15 (4): 645–96.

|

||||

1. Huang, Sherena Sheng. 2021. ‘Crypto Assets Regulation in the UK: An Assessment of the Regulatory Effectiveness and Consistency’. Journal of Financial Regulation and Compliance.

|

||||

1. Rae, Shaela W, and Lorraine Mastersmith. 2019. ‘Crypto Asset Trading in Canada: Entering a New Era of Regulation’. Banking & Finance Law Review 35 (1): 153–85.

|

||||

1. Shri T Rabi Sankar. n.d. ‘Cryptocurrencies – An Assessment’. Reserve Bank of India. Accessed 2 March 2022. https://rbi.org.in/Scripts/BS_SpeechesView.aspx?Id=1196.

|

||||

1. Zwitter, Andrej, and Jilles Hazenberg. 2020. ‘Decentralized Network Governance: Blockchain Technology and the Future of Regulation’. Frontiers in Blockchain 3. https://www.frontiersin.org/article/10.3389/fbloc.2020.00012.

|

||||

|

||||

## References

|

||||

* [@hacker_crypto-securities_2018]

|

||||

* [@azgad-tromer_crypto_2018]

|

||||

* [@ivaniuk_cryptocurrency_2020]

|

||||

* [@rae_crypto_2019]

|

||||

1. Zwitter, Andrej, and Jilles Hazenberg. 2020. ‘Decentralized Network Governance: Blockchain Technology and the Future of Regulation’. Frontiers in Blockchain 3. https://www.frontiersin.org/article/10.3389/fbloc.2020.00012.

|

||||

|

|

@ -0,0 +1,74 @@

|

|||

# What is the narrative economics of crypto assets?

|

||||

The economist Robert J. Shiller defines [narrative economics](../concepts/narrative-economics.md) as:

|

||||

|

||||

> Epidemiology of narratives relevant to economic fluctuations. The human brain has always been highly tuned towards narratives, whether factual or not, to justify ongoing actions, even such basic actions as spending and investing. Stories motivate and connect activities to deeply felt values and needs. Narratives “go viral” and spread far, even worldwide, with economic impact.

|

||||

|

||||

The phenomenon of [cryptoasset](../concepts/cryptoasset.md) and their [bubble](../concepts/bubble.md) nature is largely driven by narratives, which may differ drastically between projects. These narratives speak to different human needs and beliefs that touch upon ideas as vast as culture, [value](../concepts/value.md), money, art, law, identity and politics.

|

||||

|

||||

Bitcoin has a [narrative economics](is-narrative-economics.md) based on [libertarianism](../concepts/libertarianism.md), [regulatory arbitrage](regulatory-arbitrage.md) and aspirations of [private money](private-money.md).

|

||||

|

||||

Ethereum has a [narrative economics](is-narrative-economics.md) based on [technosolutionism](../concepts/technosolutionism.md), [libertarianism](../concepts/libertarianism.md), [regulatory arbitrage](regulatory-arbitrage.md) and aspirations of [private money](private-money.md).

|

||||

|

||||

Dogecoin is an example of a crypto asset with no political imaginaries, no [currency](currency.md) narrative, no pretense of [use value](use-value.md), no [fundamental value](fundamental-value.md), and no narrative economics whatsoever. it is a pure manifestation of the [greater fool theory](greater-fool-theory.md) with an investment thesis rooted purely in [financial nihilism](../concepts/financial-nihilism.md).

|

||||

|

||||

## Narrative Claims

|

||||

* Cypherpunk

|

||||

* Anarchism

|

||||

* [Libertarianism](../concepts/libertarianism.md)

|

||||

* [Cryptoanarchism](../concepts/cryptoanarchism.md)

|

||||

* [Financial Nihilism](../concepts/financial-nihilism.md)

|

||||

* [Post State Technocracy](../concepts/post-state-technocracy.md)

|

||||

* [Technolibertarianism](../concepts/idelogies/technolibertarianism.md)

|

||||

* [Technosolutionism](../concepts/technosolutionism.md)

|

||||

* [Technocollectivism](../concepts/techno-collectivism.md)

|

||||

* [Accelerationism](../concepts/accelerationism.md)

|

||||

|

||||

## References

|

||||

1. Shiller, Robert J. 2017. ‘Narrative Economics’. American Economic Review 107 (4): 967–1004.

|

||||